Moroccan Gross Settlement System (SRBM)

The Moroccan Gross Settlement System (SRBM) was set up in 2006.

This system, which is of paramount importance for the financial centre, allows efficient and secure transfers between participating financial institutions and helps strengthen the effectiveness of monetary policy.

The SRBM allows, in particular:

- making secure irrevocable payments through cashless settlement, using a highly secure computer system

- ensuring, by prior constitution of the provision, financial stability and reducing settlement risks likely to turn systemic

- facilitating monetary management and operation of the financial market, thus enhancing the efficiency of monetary policy management

- Finally, guaranteeing an optimum management of member institutions treasuries through a single central settlement account per participant, and where flows and liquidity are permanently monitored by Bank Al-Maghrib

Governance

The SRBM is managed and administered by Bank Al-Maghrib.

Participation in the SRBM

To take part in the SRBM, an agreement to open an SRBM central settlement account shall be signed with Bank Al-Maghrib and the technical requirements defined by it shall be respected.

Besides Bank Al-Maghrib, SRBM participant and manager, participants in this system include banks that have access to monetary policy instruments as well as certain financial institutions approved by Bank Al-Maghrib for the importance of their money market operations.

Each participant shall have a central settlement account (CSA) on the books of Bank Al-Maghrib at the Central Administration and at the SRBM subledger accounting.

The system ensures the settlement of funds transfers between participants for their own account or on behalf of their customers.

Systems of securities trading, mass clearing and credit card transactions, managed respectively by the Casablanca Stock Exchange and Maroclear, the GSIMT, an the e-money switches are considered technical participants in the SRBM through which balances resulting from these systems are settled.

Sub-participation in the SRBM

This mode is intended for institutions having a contractual relationship with a participant to process their payment orders via the SRBM. The sub-participant is accepted by the system but does not have a central settlement account.

Types of operations settled in the SRBM

The following operations are considered eligible for the system:

- Transactions processed with Bank Al-Maghrib, particularly those relating to monetary policy, cash operations in Bank Al-Maghrib branches and to coverage in dirhams of foreign currency transactions

- Funds transfer, for the instructing participant’s own account or for the account of his/her customers

- Settlement of multilateral net balances of values exchange, of transactions clearing by credit cards, and of securities transactions

- Settlement of the cash part of the securities transactions processed at the central depository Maroclear

Operating Principles

The fundamental principles of SRBM are:

- Each participant shall have a central settlement account in the system

- payment orders are irrevocable as soon as they are issued in the system

- Central Bank money is the system’s money of settlement

- Bank Al-Maghrib may grant facilities in the form of repurchase agreements with participants, under its own conditions

- Payment orders are carried out gross and in real time, in the order of receipt, and by priority

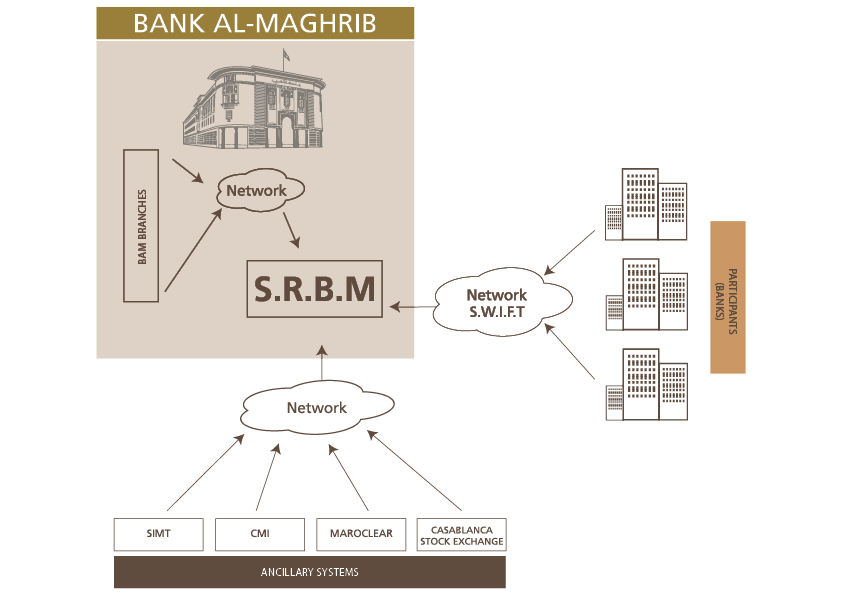

| ARCHITECTURE OF THE GROSS SETTLEMENT SYSTEM OF MOROCCO |

|---|

|

Security

Security wise, the system meets the applicable international standards, and covers the following aspects:

- Protection of equipment against unauthorized access

- Protection of applications against unauthorized access

- Protection of network against unauthorized access

- Data protection on the computer network

Thus, all users of a participant are assigned one user identification in the system and an electronic certificate. All input messages are checked to ensure their compliance. Message authentication checks the identity of the sender and the integrity of the message text.

User access control of participants includes 4 levels:

- Access to the workstation

- Access to workstation software

- Access to the application server

- Network access / management of access rights